Imogen started her first company, Qudini, after leaving university and sold the business 10 years later, 2 months before Imogen’s first child was born.

She shares some of the lessons she learned along the way in a journey that started with a hackathon she attended at age 23 where she met her Co-Founder and CTO. She will talk about her experience raising funds when she did not believe she would be a unicorn, growth hacking, choosing advisers, why she decided it was time to sell, and how she ultimately steered her business to a successful exit.

Slides

Find out more about BoS

Get details about our next conference, subscribe to our newsletter, and watch more of the great BoS Talks you hear so much about.

Transcript

Imogen Wethered

Hi everyone. My name is Imogen as introduced by Mark. So on the 11th of January, 2023 I sold my business to a NASDAQ listed company with over a billion revenue. I was thrilled, relieved, excited, very tired and eight months pregnant, and I was also very excited to get back to work and to start putting our business onto their website and keep things moving.

So I started the business in 2012, and sold it in 2023. It was exactly 10 years and six months, and it happened six weeks before the birth of my first child. So I’m going to share with you some of the learnings that I’ve had from my journey along the way, from start up through the M and A process.

My Story

So our story started in 2012, when I attended a hackathon that was sponsored by Telefonica or O2 that challenged people attending the hackathon to come up with real world solutions to so just to solve real world problems using NC technology so contactless. So I signed up on the group’s Facebook on the events Facebook group the week before the event. As a designer, I had some very basic Photoshop skills that I’d learned on a university summer holiday, and my co founder, who I didn’t know obviously would be my co founder, said we’re two developers looking to work with a designer. So I felt like I’d fraudulently represented myself as a designer, and as a result, I’d actually catfished myself a co founder from the event. And what I love about this photo. These are all pictures from DALL-E, by the way. So actually, Fraser is making the pictures, and I’m doing the coding, which I had no control over that. And the lady with the hula hoop is because at the hackathon, they had someone come around with the hula hoop to teach everyone how to hula hoop in order to keep us awake. So that was another thing that was very useful that I learned in my journey very early on was how to hula hoop

So we actually won the hackathon, and as a result, were told to apply for Telefonica tech business accelerator Huayra, which was their first version in the UK. We applied with just some very primitive ideas and pictures on some slides, and actually were outstanding to have got into the accelerator. I really think that we were their World card. So there were 20 businesses that went through. We were the youngest team, the youngest stage idea. Everyone else had some kind of MVP or even a working product of sorts.

And it was there that we then got 40k investment for 10% equity. Bit of a rip off by today’s valuation standards, but we also got office space training and mentoring from really fantastic investors and business leaders from London. They have some really great people come into the accelerator and teach us how to build a business. And then ensued, kind of 10 years of incredible hard work, as I’m sure most people know, is associated with running a business. So we started working with O2 early on in the accelerator, but it took years and years to close that deal with many near misses where they felt they didn’t need us, and then they decided they did, and then they decided they didn’t really kept us on our toes.

So we kind of knew we wanted to sell to enterprise. We took our product, basically was queue management, and later we built appointment booking software. So if you walk into an O2 store previously to us, they would have someone with a clipboard take your name and kind of manage you when it was almost your turn. With our software, you would have a tablet app that would calculate every customer’s wait time for them, and if the wait was long enough, you could take their mobile number and text them when it was their turn. And then we later layered on appointment booking on top of that.

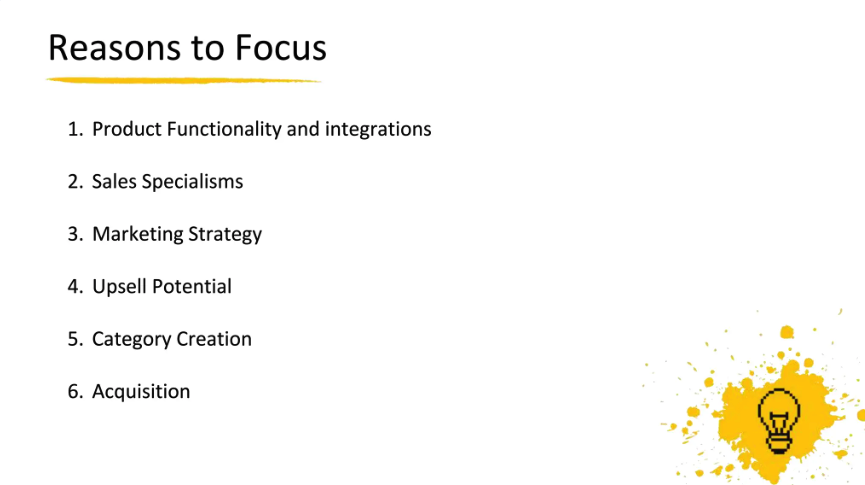

So we were trying to sell this to enterprise retail, but that was quite a difficult and long slog. So we started also trying to do a small business model for restaurants. So we actually became the leading app in Europe that were doing kind of waitlist app for restaurants. So you could go to honest burgers in London, put your name down on the wait list, and you would get a text while when your table was ready, and you could watch your place while you were waiting in the queue, but actually much later than maybe we should have done in 2019 we decided to shut down the restaurant side of the business because we just, I made a list of target acquirers, and it was then that I realized that were no particular acquirers that were going to acquire us for our retail revenues and our restaurant revenues. And even within those there were no one going to acquire us for our enterprise revenues and our SMB revenues. So at that point, I told the board that I thought we should shut down the small business model. It was met with some resistance, because over the years, many investors, many mentors, had told us we should do all sorts of models and tried to get revenue from anywhere and everywhere that we could. Mental whiplash, they call it. And we actually, over the years, I was very, very proud to say that I was very relieved that we eventually did do that focus, because it really, really helped us at the M&A side, even though it may have slowed down revenues in the year that we made that change, we then saw much greater growth later on.

And so the reason that I would advocate anyone to focus is because a the product functionality and integrations. So our restaurant app needed a completely different user interface. It needed to understand the concept of tables and the fact that this table could be two seats and then four seats and then six seats, whereas our retail version of the product needed to understand advisors and staff, and then the integrations make it harder. So within integrations, we’d need to integrate with workforce management, CRM systems in retail, whereas in restaurants, there were 1800 different POS providers. So being able to integrate with all of those was just an enormous feat in itself.

Also sales specialisms. So we found that you either have sales people who are able to do enterprise and they might have specific retail contact base, or they might be restaurant focused, so we weren’t able to find teams, and we were spreading any resources and the limited fundraising that we’d raise far too thin, particularly across marketing as well, and then also the upsell potential. So the best way that you can grow your revenues is to sell more to your existing client base than to try and sell the same thing across multiple different industries and verticals.

So we then started building out more functionality for the retail industry, and we saw that grow and by retail. I also include banks as well. We work with banks, and then category creation, which is something Joe mentioned earlier on, like playing your own game. So it was a really wise investor that once said to me when I was trying to raise funding, look, you’re trying to be too many things to too many industries, and you’re not winning any of them. You need to figure out who you are and also how you set yourself apart in that industry. So we wanted to be, at the time, just the best in queuing and appointment booking, like the number one in hotels. But we’d actually started to build out more within our space, within our product space, including task management, appointment booking, etc. But our name, Qudini, was too focused on the queuing product, so we came up with this category concept that described how we help retailers to choreograph their customers and their staff across a retail environment, retail choreography. And thereafter we put that next to our name, it went down really, really well in the industry, and it really helped us to clarify who we were and what we did and who we targeted. And then acquisition as well. So having a really focused industry and size of business with enterprise, retail and banking really helped us at the acquisition side as well.

So fundraising, so we stayed incredibly capital, reasonably capital efficient through our years, I raised about 4.4 million over the years, but sadly, it was never the positive KPI that actually it turned out to be for the business. I feel that there’s a lot in the industry that really heralds companies that raise billions of dollars of money and kind of a unicorn businesses and the VCs of the world, etc. So I always felt a need to kind of pretend to be a unicorn and go out there and pitch numbers that I really didn’t believe we’d be able to meet in order to try and raise ridiculous sums, because the VCs were so much easier to find. And it was only in kind of 2018 when actually business, we I got approached by some investors that wanted capital efficient businesses. I was like, actually, this is a good positive KPI.

So we had some kind of different levels of funding raise. So we raised from angels. Our first round was very easy. Just met them on Angel List. They didn’t even want to meet us in person. That was great. Second angel round was much, much harder. I had a angel who was a real stickler for numbers, and he wanted to see, and this was when we only had a very, very nominal amount of revenue. He wanted to see where my revenues were going to come from, by industry and by country over the next 10 years. And so as a result, my forecast model just got incredibly complicated. And I actually after that, I never managed to get the confidence to make a simpler forecast model, because I was always terrified that investors were going to ask me for these kind of metrics. Eventually, he said he would invest, but only if he had advisory shares, and he thought our valuation was too high.

Fortunately, shortly afterwards, I met some more forward thinking investors who really understand the business, and said I wasn’t raising enough money, and they’d justify double the valuation and I’d raise double the amount. So it really shows there are different types of investors that you can meet out there. And some of my key learnings from this process were that you control your timescales, not them. I should have said to them, this is when we’re closing. Are you in? Are you out? And I should have had much more confidence. And as again, Joe said, that kind of with or without you energy, this is happening. Are you on board or not? But I kind of let him lead the way. I was very nervous at it. I didn’t know what I was doing. I should have qualified and asked what the ticket size was, what his normal ticket size was, and also his expectations to be on board. And also, I’ve learned in the industry that it’s important to be wary of people that title themselves angels, because there are people that kind of go out and they’re just looking for maybe small ticket sizes, and they take for a bit of a ride, whereas, actually there are some groups out there, and you need to just find them, and it’s a lot of research.

And then for our next round, which was us, or kind of later stage, was asked 2018 series A. I knew we, the plan was to raise up to 5 million. So it was a big round. So I put them on my unicorn costume, and I went out to the VCs with my investor debt. This is a horse pretending to be a unicorn. And, yeah, I’d actually I shouldn’t have done it because I intuitively knew that we were going to raise from a VCT. So does anyone here know? Does everyone here would know what a VCT is? It’s a venture capital trust, their investors can typically benefit from EIS privileges on their own. So they’re typically they have a limited amount that they can invest in a company over its lifetime. So they’re looking for more capital efficient, typically lower risk, slightly lower returns, so three to 5x over five years or so. But as a result, they’re kind of looking for racehorses more than unicorns.

So I intuitively knew we were going to race from one of them, and eventually we did. But I’d spent a lot of time going around to VCs and and found the process very tiring had wasted my time a bit.

Key Learnings from Fundraising

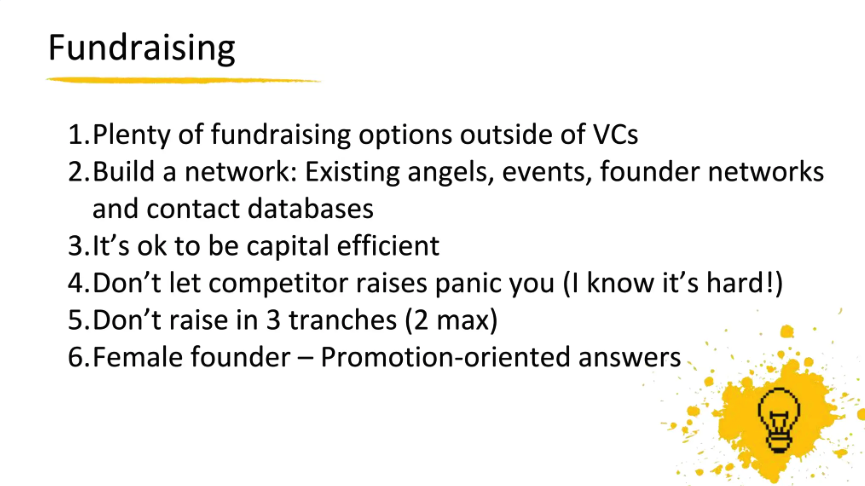

And so my key learnings overall from fundraising have been that there are plenty of fundraising options out there, outside of VCs. You just need to build a network, find your existing angels, go to events, build founder networks are incredibly important for finding people who are in their portfolios and getting introductions. And there are some also great contact databases going around there. If you kind of network around people can share you their list of investors. It’s okay to be capital efficient. And I wish I’d known this earlier, because it really, really is a strong KPI at M&A as well, which I’ll go into in a second.

Don’t let competitor raises panic you.

And this was a big one, because I’d always see like our competitors had raised 10, 20 million, and I’d panic and I’d be really, really angry for a week or so. But then over time, I started to realize that actually, they’re going to have to sell for at least 20 million or whatever they’ve raised before their founders and their early shareholders are going to make anything back. They’re going to have to grow their team significantly in order to justify that raise, and they may not hit their targets, and therefore they may need to raise more, possibly with a higher liquidation preference, that means they give up more of their more of their sale proceeds.

So I then learned that not to be super anxious by it, and just to kind of take things as we could, and manage things by our time scales, and to really just work hard and do try and be smarter. And I also found that when we’d raised more money, we were a lot less savvy with our cash. We raised some money and we thought, oh, let’s what should we name our meeting rooms? The team wanted to get a pool table to show off, and we just weren’t smart with cash. So actually, when, when everyone was like, Okay, how do we get this business working? How do we get to profit? Everyone had a lot more like higher morale, but also much harder working at the same time.

Don’t raise in three tranches. So this was a big mistake I made for our series, a we closed a advanced subscription from our angels just to get some money in. Then we raised 2 million, and our VCT Seneca partners said that they were happy to invest before we had the rest of the commitment, and then we went out to raise the rest of the money. But that meant that we did three rounds of paperwork cycles, and it’s the paperwork cycles that really take a long time. So the fundraise ended up taking a year, rather than six months, as it perhaps should have known.

And this last one is really frustrating, but female founders are asked different questions to male founders. Has anyone seen this research before? So there’s a great TED talk out there how they’ve studied some pitches from male and female founders and the questions that are asked at the end. And essentially, the male founders are asked questions that are more focused on promotion. How are you going to grow this business? How are you going to dominate the market? Whereas the female founders are asked questions that are more focused on protection. So how are you going to protect against competitors? How are you going to be able to scale something in light of this problem?

So the light at the end of the tunnel that the women are able to do better and raise more if they manage to answer those questions with promotion oriented answers. So you have to basically flip the question you’ve asked and pretend you are asked a growth promotion question. But it’s hard, and it’s a tricky skill to learn, so it’s worth watching this video and happy to share it with anyone after.

GTM and USA Scale

So after we we raised our series, a which actually we only raised half of because, because of the three tranches, we had a commitment from the final investor who then pulled out. So meanwhile, we were, we were trying to figure out how to scale in the US. So we signed up to an accelerator that we paid 20,000 pounds to be a part of. Didn’t have to give anyway any equity, and this is a racehorse going off to the US. So we joined this accelerator, and it was great. Actually, we learned some of the basics of building in the US, because we had no idea how to do that. We thought, do we set up an office? Do we build a team there? And this accelerator really helped us to clarify our thinking and plan for that.

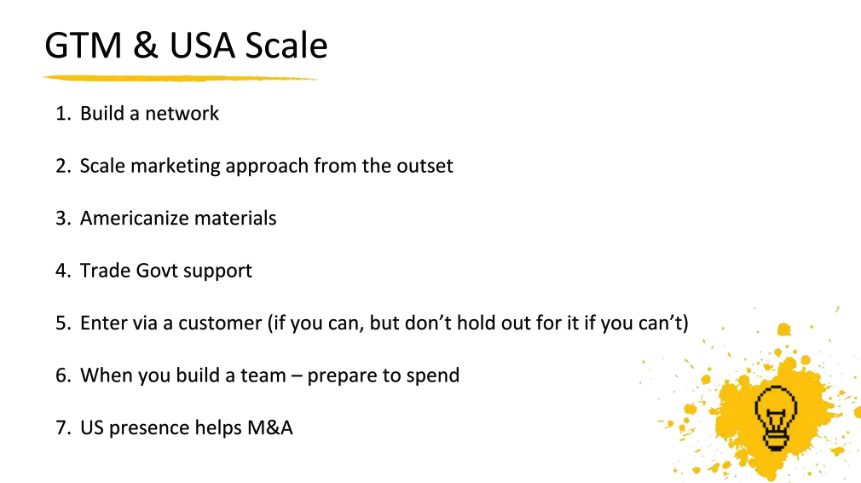

So my main learnings from this was, first of all, build a network so in person and online, like connecting with people on LinkedIn and just becoming and being in the US by osmosis, also scaling your marketing approach from the outset. So in the UK, you can do a lot more by building network with the kind of clients that you’re trying to get in contact with, in the US everything’s huge. So you need to scale from the outset. It’s hard to just gain through building a network. Everyone’s a bit more transactional than they are in the UK. So it was all about trade shows, marketing, Google ads, outbound, outreach, and really kind of scaling the approach from the outset, which is really, really helpful to learn.

Americanizing our materials from the outset. So if I were to build another business now, I would just Americanize the website from day one. First we were like, do we have a UK and then a US website, depending on where they’re visiting from. And then we realized, UK B2B businesses are so used to, used to seeing websites Americanized, that we just went and Americanized all of our content. We got some great support from trade gov in the US, so they helped us with going to events, connecting us with a few retailers as well. Another piece of advice we always had was that you should enter the US via a customer. But actually we try to do that, and it’s hard enough to gain a customer in one region that then trying to get them to then kind of being dependent on them to build you and spread you into the US is hard enough.

So actually, our first customers came via scaling our marketing approach, outreach trade shows, etc, and being present in the US. We then managed to spread that further when some of our international clients put us in their US stores. But I would say, when people tell you this, it’s great if you can do it, but don’t hold out for that.

Covid Happened

And then when you build a team, I’m sure, as all of you know, prepared to spend a lot of money. So we actually never ended up building a team in the US, COVID hit. And we found we were able to do things a lot more virtually, which saved us a lot of money, and we managed to kind of get a great foothold in the US, and that helped us with our M&A journey. And while we were kind of figuring out how to build in the US, we also started learning about I started learning about how to optimize our sales team, so this sales pod structure. So initially I’d had the sales team account, like everyone trying to do all parts of the sales journey, or at least we had lead then we separated out lead gen, but I still had people trying to close accounts and then manage accounts. Things only really started working for us when we had this sales pod structure, where essentially you have four people a closer, so someone who takes all the leads and takes them through to close of the contract maybe helps with the onboarding, building in the implementation team, not doing the onboarding, and then hands it over to an account manager, slash customer success manager, responsible for building a relationship, growing the revenues. And then with within the pod, you also have outbound sales who are getting in touch with custom new prospects, and inbound marketing who are kind of building content and keeping everything relevant. And you might have different pods for different regions, different industries, but it worked really well for us. We found that the outbound sales and inbound marketing, we could spread across multiple pods, but just making sure everyone was focusing on what they were really good at worked really, really well for us. So we started to see a lot more traction pick up then.

And then COVID hit, and actually, so we hadn’t raised our second half of our Series A, we’d had a pretty tough time, actually, pre COVID, and it was the closest I ever felt to burn out. Where I’d been slogging away trying to get things moving, but nothing was working, and we hadn’t yet seen the growth of our UX us accelerator in the sales pod structure kick in. And it was then that I learned that, for me, I’ve burnout. Some people had always said throughout 10 years, oh, don’t work too hard. You’ll burn out. And burn out if you work too hard. And actually, it was only when I was working hard, but nothing was working, that I really felt close to burnout. And so I really think that it’s when kind of when you’re doing something and it’s not moving, that’s when it can kick in.

And then so that stores started shutting down. I was walking home from work every day being like, gosh, we’re going to die, but we’re a cockroach. We always come back. I really feel like, this isn’t it? And then my other side of my head telling, no, no, this is it. This is death. There’s no way you’re coming back from any of this. And then, randomly, kind of few weeks into COVID, we got three incredible luxury retail leads come in via the website within a day. And I was like, gosh, this is weird. What’s happening? And we started to see our website traffic spike. And it turned out that with COVID, suddenly queue management software was the hottest product that anyone could want, because people were buying us like as if we were some kind of insurance product. They didn’t know if they were going to need our software when their stores opened, but they knew that they were going to have a queue, and they knew that people were going to be less akin to wanting to queue. So people started implementing our software. And then in 2022, people started implementing more and more appointment booking software.

The learning for me there was that there really are varying degrees of product market fit. You always hear about, oh, you need product market fit. And I always thought it was something you do or you don’t have, but it’s something that timing can influence, and it’s something you can have a different level of either very, very this for us was stratospheric levels at the time.

So it was after our 2019 kind of half Series A raise, that I started thinking about whether we should sell the business, because things weren’t going well. So I started inquiring more and more about M&A and how businesses sold, and then things started to get better for us, so those conversations with M&A advisors became more and more exciting, but I learned that a lot of companies actually sold through M&A advisors, and I got some introductions to M&A advisors and started To learn more and more about the M&A process, and so I spoke to them over kind of a series of two or three years, and learned a lot along the way.

M&A

Profit is Important & Capital Efficiency

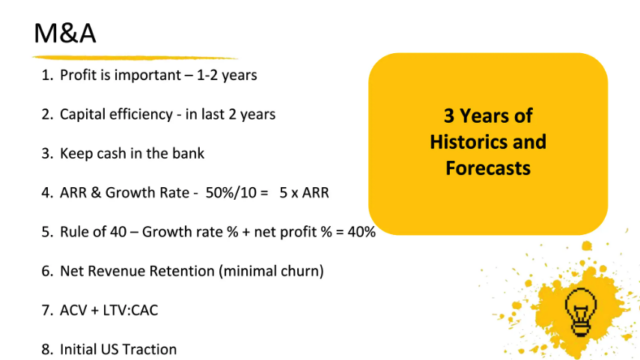

Some of my key earliest learnings were that profit is important. So one to two years of profit is very important for the business and capital efficiency, at least in the last two years. You’re not burning cash. It’s probably a couple of years on from any VC raise in that respect.

Keep Cash in the Bank

Keeping cash in the bank, because that gives you optionality. It gives you leverage, and it also gets distributed to the shareholders on sale.

ARR & Growth Rate

So I always hurdle SaaS businesses sell for five to 10 times ARR, but I never knew what the driver of that five to 10x multiple was, and I learned that it’s often defined by the growth rate. So it’s your growth rate divided by 10 times your ARR. So say your growth rate is 50% then it’s a five times ARR multiple. If you’re growing at 100% then 10x so that was a really interesting learning.

Rule of 40 & Net Revenue Retention

I also learned about the rule of 40. So which is your growth rate percentage plus your net profit should equal 40. And the levels of how with like which is more important has changed over time. So now net profit is more important, or not more important than growth rate, but it’s become more important than it was, whereas it used to just be growth rate.

ACV + LTV: CAC & Initial US Traction

So minimal churn, average contract value and your lifetime to cost of customer acquisition ratio. So. And also initial US traction, because most strategics have some kind of business in the US, and they want to see that you’re building in the US.

So these metrics are really, really important at helping me learn to optimize the business for sale.

And also about the different stages that companies get acquired at. So I learned that early stage kind of, if you’re like, you’ve got an early stage product, it’s great IP tech product. You haven’t got much or any revenues, then that’s kind of a good option for an Acqui hire. If you’re at two to 4 million revenue, then it’s much more awkward and harder to sell. If you’re at 5 million plus, then M&A advisor, like, great. That’s a good, saleable business. 10 million they’re like, great, that’s easy. So it was really good to know those benchmarks and what we were aiming for, and where we sat within that at the time and over the two years, where we got to on different levels of that journey. And then I also learned. So I’d been speaking with not just M&A advisors, but corporate dev leaders at some of the big tech companies as well to learn.

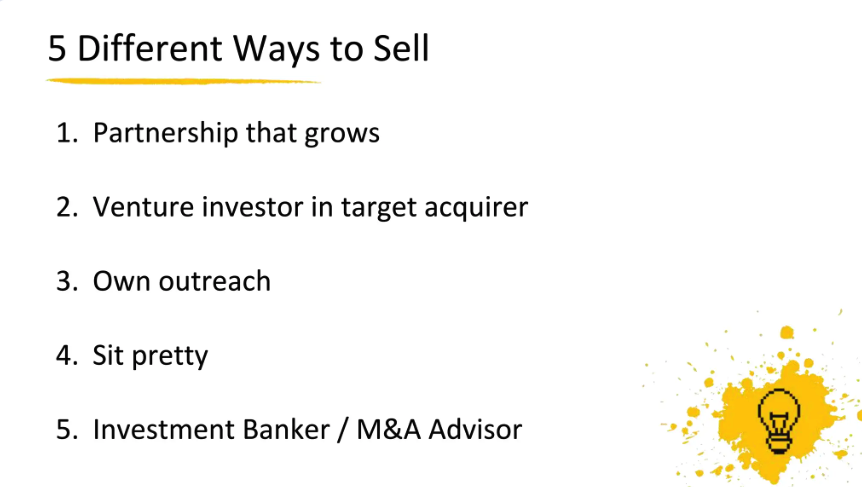

Five Different Ways to Sell

Number one, which is what people say is the best is where it’s a partnership that grows. So you embed yourself in with a potential acquirer who would be great for your software, and then they later come and knock on your door, or you build that relationship, and then they acquire you, which obviously is a dream, but it takes a lot of time to set up, and it’s also high risk. So if that company decides to acquire another company, or to build your software themselves, which I have seen happen, then you’ve invested a lot of time in that partnership. So you need to do it in a way that’s diverse, and you don’t do it with just one company.

The other is that a lot of these big companies have their own venture investments. So Cisco, SAP, Salesforce, all have venture arms, so you might get investment from them and then keep building that relationship. So similar to number one.

Number three, which some companies do do, which is their own outreach. So you might get in touch with corporate development leaders or product leaders, or the CEO or alliances teams of the acquirers that you’re going after.

Number four is sit pretty, which I thought was originally how companies got acquired, which was even kind of told to me by my board that said good companies get or great companies get bought, not sold, which is obviously great if that happens, but we don’t find the love of our life by sitting at home waiting for them to come knocking on the door.

So with us, we chose to use an investment banker or M&A advisor, and they ran a full kind of end to end sales process to take the business out to market. And I’ll take you through the steps that they they took us through, and eventually that lent ended up in our acquisition.

They taught us about the different types of acquirers that there are so and what percentage of the market they are. So I caught up with an M&A advisor before doing this talk, and this is the latest. So private equity, typically 11% of the market. PE back, strategics, 45% or trade kind of publicly listed strategics, 40% and then I’ve got some insights on the different benefits of selling to each of those and some of the risks. So feel free to come talk to me afterwards, and I can go into more detail. And can also see a summary there

Process They Took Us Through

And then this is the process that they took us through.

So first of all was materials building. So they build a kind of 100 or so page deck. So it’s like an investment deck, except you might have 10 pages on the competition, rather than just the one page you’d have in an investor deck, you also have a summary of all that data. So an exec summary, that’s just two pages a financial package, three years of historics and three years of forecast, which actually was less than we were giving investors, especially this one.

And NDAs. And then process letters, actually acquirers will also assign sign NDAs, which investors, kind of, notoriously, will refuse to do. So that was quite a nice assurance for the process as well.

And then they build a list of target acquirers. So it’s kind of a lot of private equities, but also a lot of a lot of strategics as well.

And the reason I think going with an M&A advisor is beneficial is because there’s 11,500 private equity companies in the US and the UK, and they all have different specialisms. So people that do their own outreach, it’s easier to get in touch with the strategics, because you might know who they are, but finding the private equity companies is very difficult. So that was what was great for us, as we’ve managed to get more more outreach and therefore more competitive offers.

We actually did something sneaky on the side, which is I put up LinkedIn adverts that were just on normal sales and marketing adverts, but I put an audience for the target acquirers so that I wanted them to see us before, and kind of know about our software before we were out there. And then you approach them, and then you wait, so you might go to the tier one, acquires first, and then the tier two. And then our bankers would hold the initial calls. So they’d kind of screen and understand the interest, get the NDA signed, and then they would give them the longer, kind of full deck. And after the management presentations, then they’d give them the financial package in more detail.

So after the once you’ve kind of had the calls, you set they set up the management presentations, which is where you then present a version of the sim to the investors. This was just as I went on holiday to Portugal, and the meetings just started filling in. And I couldn’t help but I thought I’d be able to sneak in a holiday. I also had terrible, terrible morning sickness, so I was kind of on the back of calls saying I’m just going to charge my laptop, and then, just like munching a cheese biscuit, just to kind of keep the nausea at bay, because if anyone over here has had morning sickness, you’ll know that you actually just need to eat all the time to stop nausea. So that was probably the most challenging holiday I’ve been on.

And after that, they then have access to the financial package. And there’s then kind of to and for questions, and then the bankers will kind of take them through a process to get indications of interest, and also letters of intent. And this is where they’re really good at controlling the time scales. So by this date, we’re expecting letters of intent. So those kind of started to come in around September, and then you negotiate over the LOI, agree the LOI with your chosen acquirer. And after that, you go into a period of exclusivity where you’re not allowed to talk to anyone else who could be a possible acquirer. And then you go through an intense due diligence process. So you’ve just got the offers, and you think you can breathe easy, and then you get this insane list of things that you have to gather. And I thought we’d prepared it because we had our fundraising due diligence folder, but it was just on another level in terms of the information that was required.

So after that, they then agree that they’re ready to go ahead, and then you go to the share purchase agreement, and there was a lot to negotiate. I was very, very surprised by how much there was to negotiate, because you think it’s just the company sale and whether there’s an earn out or not, but there are so many different things.

What to Negotiate

So first of all, definitions of things like cash, the purchase price adjustment. So when they buy you, how much do they hold back, in case things sway either way afterwards, in terms of the final bank balances, disclosure letters, and how those are negotiated, indemnities that they’re going to expect, and then escrows that they’re going to hold back, and then the earn out. So there was just a lot to negotiate. So we had to engage lawyers and also very good accountants who had experience with M&A.

And then finally completion. So that was after a kind of six to nine month process in total. So some of my kind of key tips from the process are, first of all the costs. So the advisors, lawyers, accountants, it’s significant. So you do that’s one of the reasons you need cash in the bank and to be prepared for it, because this for sale doesn’t go through, you still have to pay off some of those fees as well. Keeping your files and secretarial docs in order. I was very glad that I’d been quite diligent and made sure, like all of our finance people, were good at, kind of keeping paperwork digitally and and in storage. But I did spend at least two or three days in our storage unit just trying to track down bits of paper, preparing for tough negotiations at the end of the day. So if you’re negotiating with the US buyer, they typically the negotiations are starting at four or five o’clock, when you’re kind of in your end of day, lunch, post-lunchtime lag. I actually found it easier to negotiate in the evening than I did at kind of four or five o’clock.

What I Found Worked Best

And one of the things that I found worked best was you’ve got so many points that you need to discuss and negotiate over, and that would get quite awkward on phone calls. So we took it to ending up like writing down a document of these are all the challenges. Let’s discuss them all at a certain point, and then just sharing that document back and forth and kind of writing our responses on it. It kind of made it more seamless than just kind of long phone calls to discuss these points, gave everyone time to think about it.

One of the things that surprised me was how challenging and how your relationship with your investors and your shareholders changes for that moment in time during an acquisition. So you’re suddenly trying to negotiate with them as much as you are with the buyer, and you’re not all as aligned all the time as you might expect, finally, start the investment banker conversations early, because you can really learn how to optimize your strategy. So the investment banker I spoke to before this said that companies typically speak to him kind of three years before they get acquired, and they’ll talk to him about things like, should they replatform their technology? Because that will help them understand whether it’s a good idea or not, before M&A. Drive sales all the time, because you need to keep your growth going, and also keeping cash in the bank and profit was very valuable and important.

There’s just some tips on finding an investment banker. Making sure you’re in their sweet spot is really important, because you don’t want to be small for their size deal, and you don’t want to be too big that they don’t have the context that you’re looking for. And so these are some of the questions that I would ask them. So yeah, so that’s on my M&A journey.

Final Tips

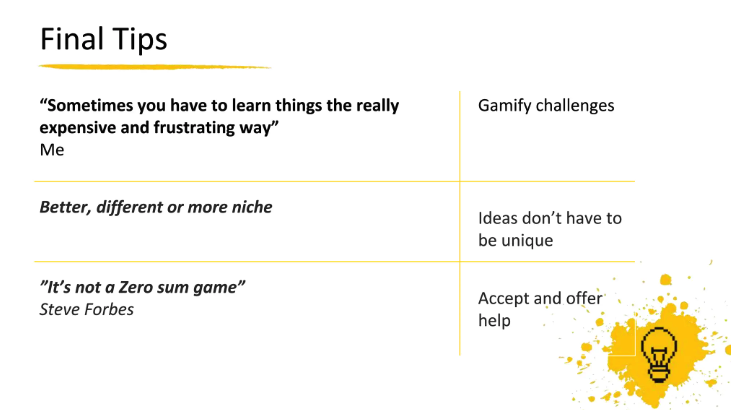

And then just kind of a few in a few kind of tips and my mantras from along the way of building a company. So luck is where preparation meets opportunity. I love this idea that actually we manufacture our own luck by working really hard and creating opportunities and finding opportunities. And I love this Brian Tracy quote, decide what you want, then act as if it were impossible to fail. So working hard and having grit is really important. And I find that in startup stories, no one ever wants to hear this. Everything has to be an overnight success, and we all want cheat sheets. But actually, everyone I’m sure knows here that it is just incredible hard work and sacrifice, but it is fun at the same time, it’s work that you love doing, and you’re learning all the time and you’re growing.

This is my personal mantra, which is gamifying challenges. Whenever I was kind of how to screw up, I’d say sometimes you need to learn things a really expensive and frustrating way to help me get over it. The fact that ideas don’t have to be unique. They can be better, different or more niche.

When we’re in Wayra, this investor came in and had this thing that the best B2C ideas are things that get people laid, paid or made, which I thought was quite funny. So I think, like just generally thinking about Maslow’s Hierarchy of Needs and how you can help consumers get that but within the B2B world just doing things better and making sure that businesses are getting a return.

And then Steve Forbes, it’s not a zero sum game. So accepting and offering help, and actually that people really like to help other people. And I love it when people ask for help, and also love to obviously ask for help, because it’s helped the business a lot.

So my journey, I hope some people might have some questions. Thank you so much all for listening.

Want more of these insightful talks?

At BoS we run events and publish highly-valued content for anyone building, running, or scaling a SaaS or software business.

Sign up for a weekly dose of latest actionable and useful content.

Unsubscribe any time. We will never sell your email address. It is yours.

Q&A

Mark Littlewood

Fabulous. Thank you. I’m going to kick off with one your initial Wayra cohort. What happened to the other ones? All dead?

Imogen Wethered

Not all dead in our cohort. I know there’s, but not sold.

Mark Littlewood

Okay, so you’re the only what you were the outlier?

Imogen Wethered

I think so, yeah.

Audience Member

Did you choose not to do it, or wasn’t needed at your size?

Imogen Wethered

Financial due diligence, oh, like a third party audit. No, we didn’t. And we were kind of told that that whatever acquirer would do significant due diligence themselves. So we and then advisor wise, we had London based law firms. Our accountants were, I think, in Kent, and then our M&A advisor was in the US, which was something that our board wanted us to do, but I actually had spoken to a lot of UK advisors who had a lot of us contact, so I don’t think that that was necessarily essential.

Audience Member

Yeah, thank you for for that. I’m sort of halfway through this process, so it’s it was really interesting, and you said, be prepared for really tough negotiation. What was the, what was the toughest thing that you had to negotiate? Or if you could kind of give yourself, your past self, some advice on where you could have helped, you know, been stronger, or held a held a firmer line.

Imogen Wethered

It’s really hard. Like all the all the negotiations were pretty tough, but what I was surprised by was how tough the internal negotiations were, because you’re you become the messenger, and the board were like, go back and get these terms. And you’re like, I can’t. I’ve already tried that, but then they want you to go back. And that’s why I found the document quite helpful, because then it was proof, and I would send it to them and say, Look, this is what they said. It’s not just me. And that helped them come round to the idea far, to their way of thinking faster, and we could somehow get to the middle. Yes.

Mark Littlewood

Soryy. Yes.

Audience Member

Hi. So I’ve got two questions. The first one is around when you talk about the growth rate, so what growth are we talking about? Are we talking about customer growth rate, revenue growth rate, like, what specific growth rate is being looked at? That’s the one part.

And the second part is, from an IP perspective, how much of an impact I don’t know where your IP resided, but how much of an impact did that also have on the interest from acquirers in terms of actually looking at what you had and the jurisdiction in which that RP SAT?

Imogen Wethered

Great, okay. Growth rate for us was all about annual recurring revenue. So basically, whatever our total contract values were and how fast that was growing, and the lower the amount of churn we were having. And then with IP, so our software wasn’t very protectable at all. So for us, it was all about just kind of the customers we had, the brand that we’d created around it, or the and the they loved the product and how it looked, and we had a great interface, etc, but nothing within there was protectable.

Mark Littlewood

Yeah, I run that. Sorry, the right hand corner.

Audience Member

I’m interested to know how transparent all of this was within the business. So how did you manage your team and the rest of the business? At what point did you break cover and say, We’re selling the business? I’m just really interested to get insight.

Imogen Wethered

Good question. So the management team, kind of commercial director, CTO finance, obviously they knew, and they knew it was in my plan for kind of two years. The rest of the company, we kind of only told in the month before it was about to close, unless they had to get involved in due diligence, then they might have known kind of two or three months before, if they were providing information.

Audience Member

They take that and are they still part of the business.

Imogen Wethered

So quite a few people are but a few people do leave. So I probably say it was about 25% that moved on. It’s interesting because one on the one hand, they’re scared about losing their job, and then the second hand, they then go searching for more jobs because they’re not sure they want to stay. And it’s like, which do you want? Do you want to stay or go? Because I’m very confused. So they, I think people just get confused and and they think that there’s no opportunity for them and that they’re going to be let go. But actually, the people who have stayed have got really good progress and kind of improved their careers. And I it was a shame, I think, for the people that did move on.

Audience Member

Thank you.

Mark Littlewood

That’s a great question. There’s another question over here.

Thank you. That was really interesting. Going back to the question about negotiation, did you do that yourself?And is that sort of common practice, or do sometimes sort of external people and step in and do it for like an advisor.

Imogen Wethered

So that’s the M&A advisors role, but you do inevitably end up getting involved and starting so it was me who was kind of building out these are all the points that are a problem, and then sharing that document and just having that conversation direct. I just think, and every founder relationship, even where they’ve used an M&A advisors, you do end up getting involved in some way and negotiating direct.

Mark Littlewood

Great question, what’s next?

Imogen Wethered

I don’t know.

Mark Littlewood

How long ago did you make the sale?

Imogen Wethered

Was a year and a half.

Mark Littlewood

Right, so you’re super happy doing what you’re doing for another year and a half. Have you thought beyond that particular date? Was it a three year time?

Imogen Wethered

It’s three years. Yeah, it’s it’s interesting. I’m learning a lot. It’s great to be working with the US company, because I’m learning about how to build in the US. We got to do things like go to trade shows, where previously I’d just been kind of freeloading my way around on other partner stands. We actually got to go this year with a stand that we’d spent money on, and get to see how these things actually generate leads so that that I’m finding really interesting and useful. It is a different experience, though. You’re suddenly kind of being told how to do something that you’ve done all the time, and feel somewhat like being back at school when you’ve just had a really long summer holiday. So, and I don’t know, I think I want to start another business. I don’t think I’m ready to quite yet. It’s a lot I’m more because of the fundraising side. I think that’s what I’m not excited about doing it again for a while.

Mark Littlewood

So for you was the fundraising the thing that, because you obviously really got into the growth stuff, and didn’t talk as much about that as we have in the in the past, this really interesting stuff that you should speak to Imogen, about about that as well, and and Duane, in fact, who’s a master at this. But it’s that, do you think you would if you did another business? Would you self fund it for as long as possible?

Imogen Wethered

That I also think about, and I’m not sure, because it’s I think I’d definitely try and bootstrap it for a year or so, because, I mean, in the first year of our business, we ended up giving away 10% then 20% for really not a lot of money. So I definitely try and avoid doing that, but I think eventually raise money to grow it. And just the question is, what type of businesses, whether I’d want to build something that would be a unicorn or actually just happy doing something again, like we did good racehorse.

Mark Littlewood

Josh.

Audience Member

Yep. So I think a lot of people underestimate the psychological toll it takes on you and the emotional toll. Did you have a person that you could confide in outside of the business, outside of your board and your people that you got to talk to and use as a sounding board?

Imogen Wethered

Yes, I did. First of all, my husband, who’s been amazing and was also very good at making me focus on the one thing, like, will it help you sell the company? And I was like, okay, yeah, that’s the most important thing. But also just kind of a series of advisors throughout the business lifetime. Some focus on sales, some who are great at helping with investment, and then some who were really useful and friends, mostly during the M&A process, who’d done it before, one who gave me a very good tip increase your salary before you sell, because it’s very hard to do that afterwards.

Imogen Wethered

So, yeah, but it is hard work, and it’s, it’s funny speaking to founders now who have sold, because you do go through a bit of kind of pro trauma processing after you’ve sold, where you’re like, when you realize, like, quite how much work it is, and you have a bit of an identity crisis, because you’re not quite sure what to do much because it is, was such a traumatic and challenging journey.

Mark Littlewood

One final question?

Audience Member

Stepping on what you just said. If you now think I can pull it off in five years, do you think that’s doable? Based on the experience you’ve gained, or.

Imogen Wethered

Could do it again in five years?

Audience Member

Yeah.

Imogen Wethered

Possibly. It would, I think it was the product build and the customer base, and if you’re doing enterprise sales, I’d maybe say six or seven. I think, yeah, with the experience, and I also think AI is going to make things like fun, creating the investor deck so much quicker that I wouldn’t have taken me six months. It might have taken me three months or four months or something. So yes, but maybe not five, but I’m up for the challenge.

Mark Littlewood

Imogen, thank you.

Imogen Wethered

Thank you, everyone.

Imogen Wethered

Founder & CEO, Qudini

Imogen was CEO and Co-Founder of Qudini, a B2B SaaS company selling queue management and appointment software to retailers and banks.

The company was acquired by Verint in 2023, Imogen is now working at Verint running GoToMarket Strategy for Qudini’s “Retail Choreography” products within Verint, a global publicly listed enterprise SaaS company.

Having started and sold a company early in her career, Imogen is a big believer and supporter in helping entrepreneurs to start young when risks are low and there’s time to learn and sell multiple businesses.

Next Events

BoS Europe 2025 🇬🇧

🗓️ 31 March – 1 April 2025

📍 Cambridge, UK

❗️3 weeks to go

Spend 2 days with other smart people in a supportive community of SaaS & software entrepreneurs who want to build great products and companies.

BoS USA 2025 🇺🇸

🗓️ 6-8 October 2025

📍 Raleigh, NC

❗️Early bird ticket available

Learn how great software companies are built at an extraordinary conference run since 2007 to help you build long term, profitable, sustainable businesses.

Want more of these insightful talks?

At BoS we run events and publish highly-valued content for anyone building, running, or scaling a SaaS or software business.

Sign up for a weekly dose of latest actionable and useful content.

Unsubscribe any time. We will never sell your email address. It is yours.